Introduction

Most of us swipe, tap, or insert a card several times a week without thinking much about what actually happens behind the scenes. Yet many people still wonder how does a debit card work and what happens between the moment you pay and the money leaving your bank account.

If you’ve ever paid for groceries, withdrawn cash from an ATM, or shopped online using a bank card, you’ve already used the technology that powers debit cards. What feels like a simple tap actually triggers a complex chain of digital communication between banks, payment networks, and merchants.

Understanding how does a debit card work isn’t just about curiosity—it can help you manage your money better, avoid overdrafts, and protect yourself from fraud. In this guide, we’ll explore everything from the basics of debit card transactions to security features, fees, and real-world examples that make modern banking possible.

What Is a Debit Card

A debit card is a payment card issued by a bank or financial institution that allows you to spend money directly from your checking account.

Unlike credit cards, which borrow money from a lender, debit cards only allow you to spend funds that already exist in your bank account.

In simple terms, when you pay with a debit card:

- The money comes directly from your bank account

- The transaction is processed electronically

- The balance in your account decreases immediately or within a few hours

Most debit cards today include:

- EMV chip technology

- Contactless tap-to-pay capability

- PIN security

- Magnetic stripe for compatibility

Because of their convenience and simplicity, debit cards have become one of the most widely used payment methods worldwide.

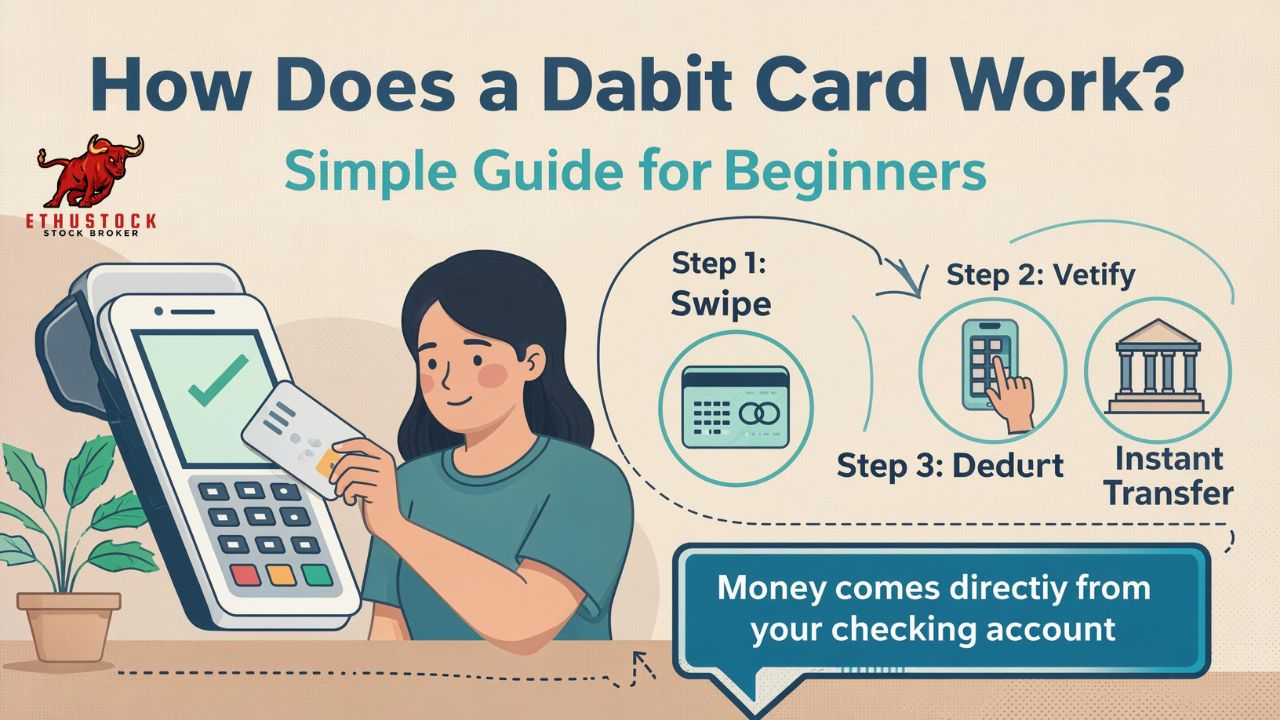

How Does a Debit Card Work in Everyday Transactions

To truly understand how does a debit card work it helps to follow what happens when you make a purchase.

Imagine you’re buying coffee at a café.

Step-by-Step Example

- You insert or tap your debit card on the payment terminal.

- The terminal reads your card details.

- The merchant sends the transaction request to the payment processor.

- The processor contacts your bank.

- Your bank verifies that you have enough funds.

- The transaction is approved or declined.

- The money is deducted from your account.

All of this typically happens in 2–5 seconds.

Modern banking networks are incredibly fast and secure, allowing millions of transactions to occur simultaneously around the world.

How Debit Card Payments Are Processed

Debit card transactions rely on a large payment ecosystem that connects several players.

The Main Participants

| Participant | Role |

|---|---|

| Cardholder | The person using the debit card |

| Merchant | The store accepting the payment |

| Payment Processor | Handles communication between banks |

| Card Network | Visa, Mastercard, etc. |

| Issuing Bank | Your bank that issued the card |

The Transaction Flow

- Authorization Request

Merchant sends a payment request. - Bank Verification

Your bank checks your account balance. - Approval or Decline

Bank approves if funds are available. - Settlement

Money moves from your account to the merchant’s bank.

Authorization vs Settlement

Many people don’t realize these are two different stages.

- Authorization: Confirms funds exist

- Settlement: Transfers money later (usually same day)

This is why some payments appear as “pending transactions.”

How Does a Debit Card Work for ATM Withdrawals

Another common question is how does a debit card work when withdrawing money from an ATM.

ATM transactions work similarly to store payments but include additional verification.

ATM Withdrawal Process

- Insert your debit card.

- Enter your PIN.

- Select withdrawal amount.

- Bank verifies your balance.

- ATM dispenses cash.

The ATM communicates directly with your bank’s system through secure banking networks.

ATM Limits

Most banks impose daily limits such as:

- $300 – $1000 per day

- Depends on account type and bank policies

This helps prevent fraud and large unauthorized withdrawals.

Types of Debit Cards Explained

Debit cards come in several forms depending on the bank and payment network.

Standard Bank Debit Cards

Issued with checking accounts and used for:

- ATM withdrawals

- POS payments

- Online purchases

Contactless Debit Cards

Allow tap payments using NFC technology.

Benefits include:

- Faster checkout

- Less physical contact

- Increased convenience

Prepaid Debit Cards

Not linked to a bank account.

Instead, users load money onto the card in advance.

Common uses:

- Travel spending

- Gift cards

- Teen banking

Virtual Debit Cards

Digital versions used for online purchases.

They improve security by:

- Hiding real card numbers

- Preventing fraud

Debit Card vs Credit Card

Many people confuse debit and credit cards.

Here’s a simple comparison.

| Feature | Debit Card | Credit Card |

|---|---|---|

| Money Source | Bank account | Borrowed money |

| Interest | None | Interest may apply |

| Spending Limit | Account balance | Credit limit |

| Debt Risk | Low | Higher |

| Credit Score Impact | No | Yes |

Understanding this difference is essential when learning how does a debit card work in financial management.

Debit cards promote spending discipline because you can only spend what you already have.

Benefits of Using Debit Cards

Debit cards have grown in popularity for several reasons.

1. Easy Access to Money

You can withdraw cash or make payments instantly.

2. No Interest Charges

Since the money is yours, there’s no borrowing involved.

3. Budget Control

Debit cards naturally prevent overspending.

4. Wide Acceptance

Debit cards work worldwide at:

- Retail stores

- Restaurants

- ATMs

- Online stores

5. Instant Transaction Records

Banks track every purchase in real time.

Potential Risks and Drawbacks

Although debit cards are convenient, they also come with potential downsides.

Overdraft Fees

If your bank allows overdrafts, transactions may still go through even without enough balance.

Fraud Risks

If someone steals your card details, they may attempt unauthorized transactions.

Limited Consumer Protection

Credit cards usually provide stronger fraud protection.

ATM Fees

Using out-of-network ATMs may trigger charges.

Debit Card Security and Fraud Protection

Banks invest heavily in security to protect debit card users.

Understanding how does a debit card work also means knowing how your money stays protected.

Key Security Technologies

EMV Chip

Harder to clone than magnetic stripes.

PIN Verification

Adds an extra authentication layer.

Fraud Monitoring

Banks track suspicious activity.

Two-Factor Authentication

Used for online payments.

Real-Life Example

If you suddenly use your card in another country, your bank may temporarily block it and send a fraud alert.

This protects your account from potential theft.

Tips for Using Debit Cards Safely

Protecting your debit card is essential for financial security.

Practical Safety Tips

- Never share your PIN

- Use secure ATMs inside banks

- Enable transaction alerts

- Monitor bank statements regularly

- Avoid public Wi-Fi when shopping online

Also consider enabling daily spending notifications through your banking app.

Frequently Asked Questions

How does a debit card work when paying online?

When you shop online, the payment gateway securely sends your card details to the bank. The bank verifies the funds and approves the transaction.

Does a debit card charge interest?

No. Debit cards do not charge interest because you are spending your own money.

Can a debit card build credit score?

Generally no. Debit card transactions do not affect your credit history.

What happens if I don’t have enough money?

The transaction may be declined or processed as an overdraft depending on your bank settings.

Is it safe to use debit cards online?

Yes, especially when using secure websites with HTTPS encryption and two-factor authentication.

Can someone steal money using my debit card number?

Unfortunately yes, but banks usually detect suspicious transactions and may refund fraudulent charges if reported quickly.

Why are some transactions pending?

Pending transactions occur when authorization is approved but the final settlement has not yet occurred.

Are debit cards accepted internationally?

Most debit cards linked to major payment networks like Visa or Mastercard work worldwide.

Conclusion

Debit cards have transformed the way people manage everyday spending. What once required cash or checks now happens instantly with a simple tap or swipe. Understanding how does a debit card work reveals the powerful banking infrastructure operating quietly behind every transaction.

From ATM withdrawals to online shopping, debit cards connect your bank account directly to the global payment network. They offer convenience, speed, and real-time financial control—making them one of the most practical tools for modern personal finance.

By using debit cards responsibly, monitoring your transactions, and following basic security practices, you can enjoy the benefits of digital payments while keeping your money safe.