Introduction

Have you ever wondered what really happens when you swipe or tap your credit card at a store? Many people use credit cards every day without fully understanding how does a credit card work behind the scenes. It might feel like magic—buy something now and pay later—but there’s actually a detailed financial system operating in the background.

Credit cards are one of the most widely used financial tools in the world. According to global banking reports, billions of credit cards are currently active, and they power a huge portion of everyday spending—from groceries and fuel to online shopping.

Understanding how does a credit card work isn’t just helpful—it’s essential for managing money responsibly. When used wisely, a credit card can help build a strong credit history, offer purchase protections, and even provide rewards. But when used carelessly, it can lead to high interest debt and financial stress.

In this guide, we’ll break everything down in simple terms—from credit limits and billing cycles to interest rates and payment strategies—so you can confidently understand and use credit cards the right way.

What Is a Credit Card?

A credit card is a financial tool issued by banks or financial institutions that allows you to borrow money to make purchases. Instead of paying immediately from your bank account, the bank temporarily pays the merchant on your behalf.

You then repay that borrowed amount later—either in full or partially.

In simple terms, a credit card functions as a short-term loan for everyday spending.

Unlike debit cards, which pull money directly from your bank account, credit cards allow you to spend first and pay later.

How Does a Credit Card Work?

At its core, how does a credit card work is fairly simple: the bank lends you money for purchases, and you repay it later according to your billing cycle.

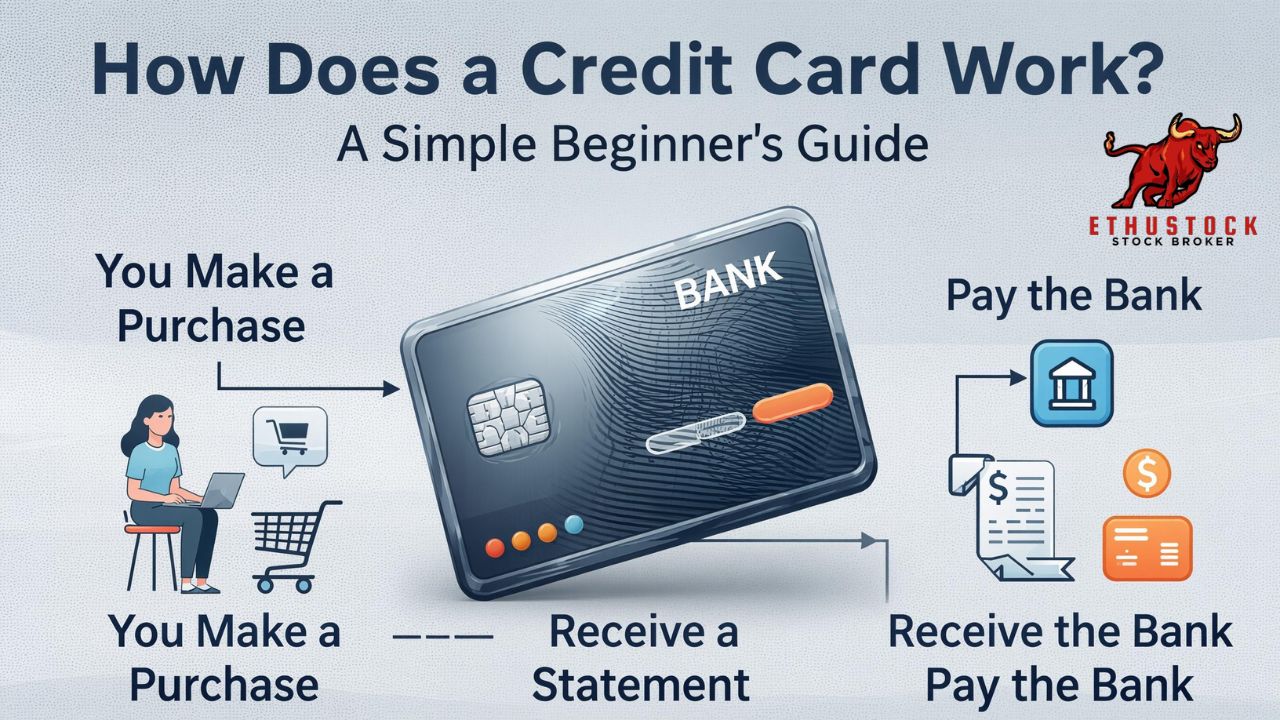

Here’s a simplified breakdown of the process:

- You make a purchase using your credit card.

- The credit card network approves the transaction.

- The issuing bank pays the merchant.

- The purchase is added to your credit card balance.

- You receive a monthly statement.

- You repay the balance either fully or partially.

If you pay the entire statement balance before the due date, you typically avoid interest. However, if you carry a balance, interest charges begin accumulating.

Understanding how does a credit card work helps you avoid unnecessary fees and debt.

The Key Components of a Credit Card

Credit cards include several important features that determine how they operate.

Credit Limit

Your credit limit is the maximum amount you’re allowed to borrow.

For example:

| Credit Limit | Current Balance | Available Credit |

|---|---|---|

| $5,000 | $1,200 | $3,800 |

The remaining amount is called your available credit.

Billing Cycle

A billing cycle is typically 28–31 days. During this time, all purchases and payments are recorded.

At the end of the cycle, the bank generates your statement.

Statement Balance

The statement balance is the total amount you owe for that billing period.

Minimum Payment

This is the smallest payment required to keep your account in good standing.

However, paying only the minimum usually results in interest charges.

Credit Card Transaction Process Explained

When you swipe your credit card, the transaction happens within seconds—but several institutions are involved.

Step-by-Step Transaction Flow

- Customer uses the credit card.

- Merchant sends the transaction request.

- Payment processor forwards the request.

- Card network (Visa/Mastercard) verifies details.

- Issuing bank approves or declines the transaction.

If approved, the purchase is completed.

This entire system operates in seconds, allowing seamless global payments.

Credit Card Billing Cycle and Payments

Your billing cycle determines when payments are due and how interest is calculated.

Typical Billing Timeline

| Stage | What Happens |

|---|---|

| Day 1 | Billing cycle begins |

| Day 30 | Statement generated |

| Day 30–50 | Grace period |

| Day 50 | Payment due date |

If you pay the full balance during the grace period, no interest is charged.

Understanding how does a credit card work during billing cycles can help you avoid unnecessary charges.

Interest Rates and APR Explained

Interest is the cost of borrowing money.

The interest rate on credit cards is typically called APR (Annual Percentage Rate).

For example:

| Balance | APR | Interest Cost |

|---|---|---|

| $1,000 | 20% | $200 per year |

However, credit card interest is usually calculated daily.

That means carrying a balance can quickly increase your total debt.

Credit Limits and Available Credit

Your credit limit is determined by factors like:

- Income

- Credit history

- Debt levels

- Payment behavior

Banks may increase your credit limit over time if you use your card responsibly.

Keeping your credit utilization low—generally under 30%—helps maintain a healthy credit score.

Credit Card Rewards and Benefits

Many credit cards offer incentives to encourage spending.

Common rewards include:

- Cashback

- Travel points

- Airline miles

- Purchase protection

- Fraud protection

- Extended warranties

For example, a card might offer 2% cashback on groceries or airline miles for travel purchases.

These rewards make credit cards more attractive compared to cash payments.

Fees Associated With Credit Cards

Credit cards may include several fees depending on the issuer.

Common Credit Card Fees

- Annual fees

- Late payment fees

- Cash advance fees

- Foreign transaction fees

- Balance transfer fees

Some premium cards charge annual fees but offer travel benefits and rewards.

Personal Background: How Credit Cards Became a Modern Financial Tool

Credit cards didn’t always exist in their current form.

The modern credit card system began in the 1950s when the Diners Club card was introduced. It allowed customers to dine at restaurants without carrying cash.

Soon after, banks and financial institutions recognized the potential of revolving credit systems.

Visa and Mastercard networks later expanded globally, creating a unified payment infrastructure.

Today, credit cards power trillions of dollars in annual transactions and play a critical role in modern financial systems.

They’ve evolved from simple payment cards into powerful financial tools that influence credit history, borrowing ability, and even career opportunities.

Smart Ways to Use Credit Cards Responsibly

Knowing how does a credit card work helps you avoid financial mistakes.

Responsible Credit Card Habits

- Pay the full balance every month

- Keep credit utilization below 30%

- Monitor statements regularly

- Avoid unnecessary cash advances

- Use rewards strategically

These practices help maintain strong financial health.

Common Credit Card Mistakes to Avoid

Many people fall into debt because of common credit card mistakes.

Major Pitfalls

- Paying only the minimum balance

- Missing payment deadlines

- Maxing out credit limits

- Ignoring interest rates

- Using cards for unnecessary spending

Avoiding these mistakes can save thousands of dollars over time.

How Credit Cards Affect Your Credit Score

Your credit card usage significantly impacts your credit score.

Important factors include:

Payment History (35%)

Paying bills on time improves your score.

Credit Utilization (30%)

Using too much of your available credit can hurt your score.

Credit Age

Older credit accounts strengthen your financial profile.

When used correctly, credit cards can help build strong financial credibility.

FAQ

How does a credit card work when you make a purchase?

When you use a credit card, the bank pays the merchant first. The amount is then added to your card balance, and you repay it later during your billing cycle.

Do you have to pay interest on credit cards?

You only pay interest if you carry a balance after the payment due date. Paying the full balance during the grace period avoids interest.

What happens if you only pay the minimum balance?

Paying only the minimum keeps your account active but adds interest to the remaining balance.

Can using credit cards build credit?

Yes. Responsible usage—especially paying on time—can improve your credit score.

What is a credit limit?

A credit limit is the maximum amount you’re allowed to borrow using your credit card.

Are credit cards safe to use online?

Most credit cards offer fraud protection, making them safer than many other payment methods.

Why do banks offer credit cards?

Banks earn money through interest charges, transaction fees, and merchant processing fees.

Can you withdraw cash from a credit card?

Yes, through a cash advance—but it usually comes with higher fees and interest rates.

Conclusion

Understanding how does a credit card work is one of the most important steps toward better financial management. Credit cards are powerful tools that allow consumers to make purchases conveniently, build credit history, and access rewards programs.

However, they must be used responsibly. High interest rates, late fees, and overspending can quickly turn a helpful financial tool into a source of debt.

The key is simple: spend wisely, track your balances, and pay your statement in full whenever possible. When used with discipline and awareness, credit cards can become valuable allies in achieving long-term financial stability.