Introduction

Choosing where to invest your hard-earned money can feel overwhelming. Between fees, fund options, technology platforms, and customer service, every detail matters. When it comes to fidelity vs vanguard, the debate often sparks strong opinions among long-term investors.

Both companies have built loyal followings and decades-long reputations for helping people grow wealth. But they’re not identical. The right choice depends on your goals, experience level, and how hands-on you want to be. In this guide, we’ll break down everything that matters so you can decide with confidence.

Whether you’re opening your first Roth IRA or managing a six-figure portfolio, understanding the differences between these investment giants can shape your financial future.

Company Overview

Before diving deep into fidelity vs vanguard, it helps to understand their origins and philosophies.

Fidelity: Innovation Meets Accessibility

Founded in 1946, Fidelity Investments has grown into one of the largest financial services companies in the world. It’s known for:

- A wide range of mutual funds and ETFs

- Active and passive investing options

- Robust trading platforms

- Strong customer support

Fidelity often appeals to investors who want flexibility, powerful tools, and diverse product offerings.

Vanguard: The Low-Cost Pioneer

Vanguard, founded in 1975 by John C. Bogle, revolutionized investing with the creation of the first index fund for individual investors. Its core philosophy is simple: keep costs low and pass savings to investors.

Vanguard is famous for:

- Ultra-low expense ratios

- Index investing leadership

- Investor-owned structure

- Long-term, disciplined approach

When discussing fidelity vs vanguard, Vanguard’s commitment to cost efficiency is always front and center.

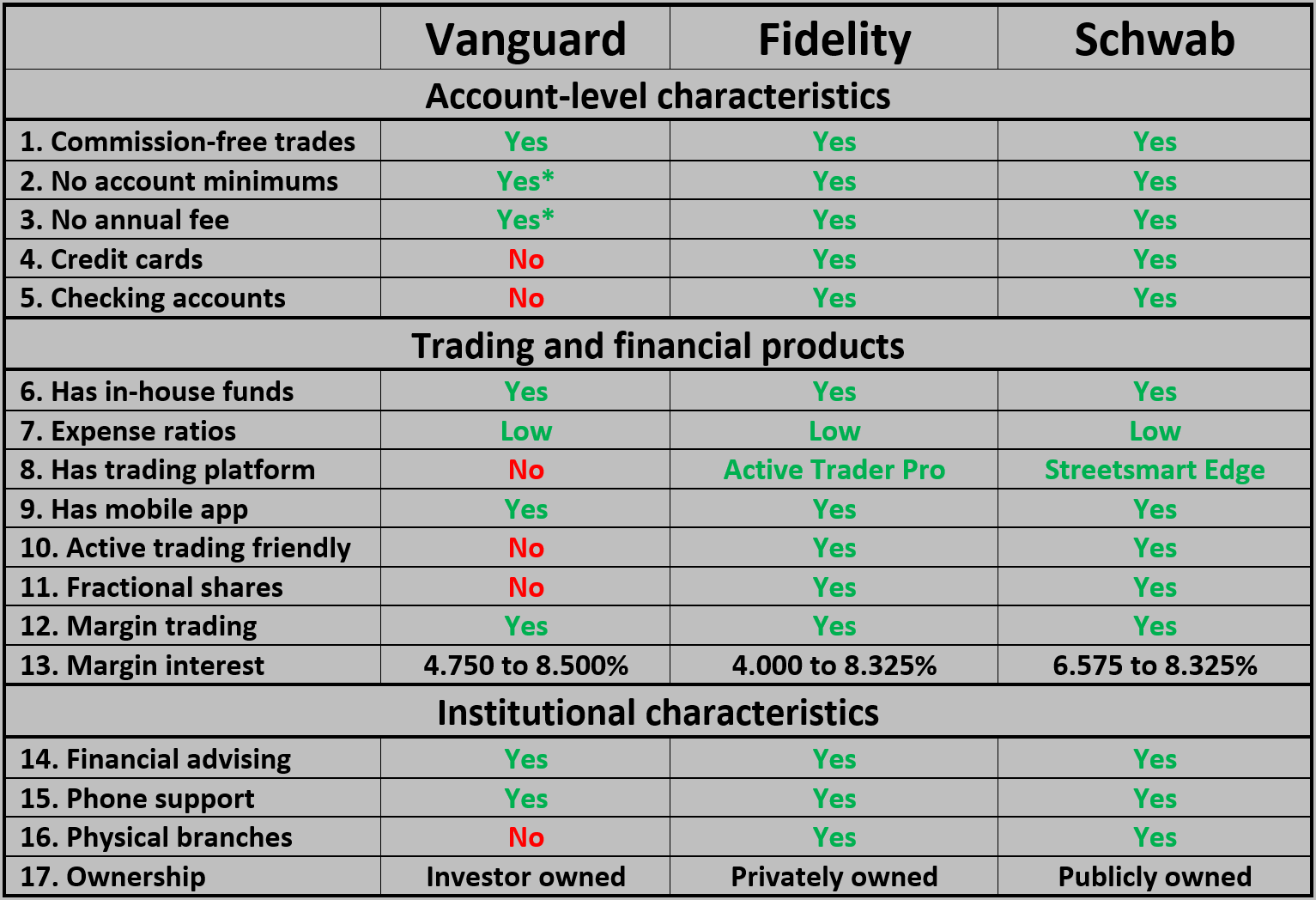

Fees and Expense Ratios

Fees might seem small, but over decades, they compound just like returns.

Mutual Fund Expense Ratios

Vanguard is widely known for rock-bottom expense ratios, especially in its index funds. Many of its flagship funds charge as little as 0.03% annually.

Fidelity competes aggressively here. In fact, Fidelity introduced zero-expense-ratio index funds (FZROX and others), which charge 0.00%.

So in the fidelity vs vanguard debate on fund costs, both are extremely competitive. Fidelity’s zero-cost funds are impressive, but Vanguard’s broad lineup of low-cost ETFs gives it consistency across the board.

Trading Fees

Both Fidelity and Vanguard offer:

- $0 commissions on online stock and ETF trades

- No account minimums for brokerage accounts

However, Fidelity tends to provide slightly more advanced trading tools for active investors.

After two paragraphs discussing costs, here’s a helpful visual comparison.

Investment Options and Fund Variety

When comparing fidelity vs vanguard, investment breadth matters.

Index Funds and ETFs

Vanguard pioneered index investing and still dominates with its Total Stock Market and S&P 500 funds. Its ETFs are widely used by long-term investors.

Fidelity, however, offers:

- A broad lineup of index funds

- Actively managed funds

- Sector-specific ETFs

- Zero-expense index funds

Both firms provide strong passive investing choices, but Fidelity’s product diversity can feel more expansive.

Actively Managed Funds

If you prefer professional fund managers attempting to beat the market, Fidelity has a deeper bench of actively managed mutual funds.

Vanguard does offer active funds, but its strength lies in passive investing.

For investors deciding between fidelity vs vanguard, your belief in active versus passive strategies may influence your choice.

Account Types and Retirement Planning

Both companies support:

- Traditional IRAs

- Roth IRAs

- SEP IRAs

- 401(k) rollovers

- Taxable brokerage accounts

- 529 college savings plans

However, Fidelity’s user interface for retirement calculators and goal planning tools tends to be more intuitive and detailed.

Vanguard emphasizes simplicity and long-term discipline rather than flashy tools.

Trading Platform and Technology

Technology can significantly shape your investing experience.

Fidelity’s Technology Edge

Fidelity offers:

- Advanced charting tools

- Real-time data

- Research reports

- Mobile app functionality

- Active Trader Pro platform

For hands-on investors, Fidelity’s tech feels modern and powerful.

Vanguard’s Platform

Vanguard’s interface is clean and simple but less sophisticated for active trading. It works well for buy-and-hold investors.

In the fidelity vs vanguard comparison, tech-savvy traders may lean toward Fidelity.

Customer Service and Support

Customer support matters, especially during market volatility.

Fidelity is consistently ranked high for:

- 24/7 phone support

- Branch locations

- Online chat availability

Vanguard also provides strong service but typically has fewer physical branches.

When evaluating fidelity vs vanguard, investors who value live support may prefer Fidelity.

Minimum Investment Requirements

Historically, Vanguard required higher minimums for certain mutual funds. Today:

- Vanguard index funds often require $3,000 minimum

- Vanguard ETFs have no minimum beyond share price

- Fidelity mutual funds often have $0 minimums

This makes Fidelity slightly more accessible for beginners.

Performance: Does It Really Differ?

Over long time horizons, index funds tracking the same benchmark (like the S&P 500) perform nearly identically.

So in fidelity vs vanguard performance comparisons:

- Index fund returns are very similar

- Expense ratios slightly influence net returns

- Active fund performance varies by manager

In truth, differences are often marginal for passive investors.

Tax Efficiency

Vanguard’s ETF structure has historically provided strong tax efficiency, thanks to its unique patent on ETF share classes.

Fidelity’s ETFs are also tax-efficient, but Vanguard has long been known for minimizing capital gains distributions.

In taxable accounts, this factor can influence the fidelity vs vanguard decision.

Who Should Choose Fidelity?

Fidelity may be ideal if you:

- Want advanced trading tools

- Prefer active management options

- Value zero-expense index funds

- Need strong customer service access

- Are a beginner with small starting capital

Who Should Choose Vanguard?

Vanguard may suit you if you:

- Believe strongly in index investing

- Want ultra-low, consistent expense ratios

- Prefer long-term buy-and-hold strategy

- Appreciate investor-owned company structure

- Value simplicity over features

Behavioral Considerations

Interestingly, one of the most overlooked aspects of fidelity vs vanguard is behavioral discipline.

Vanguard’s simpler platform may actually reduce overtrading. Fidelity’s powerful tools, while impressive, could tempt frequent trading.

For long-term wealth building, simplicity often wins.

Real-World Example: A $10,000 Investment Over 30 Years

Imagine investing $10,000 in a low-cost S&P 500 index fund at either company.

Assume:

- 7% average annual return

- Expense ratio difference of 0.02%

After 30 years, the difference in total value would be relatively small—often just a few hundred dollars.

In the fidelity vs vanguard conversation, the practical difference for passive investors can be minimal.

Frequently Asked Questions

FAQ

Is Fidelity better than Vanguard for beginners?

Fidelity may be more beginner-friendly due to $0 minimum funds and strong customer support, though Vanguard is also simple and effective.

Which has lower fees, Fidelity or Vanguard?

Both offer extremely low fees. Fidelity has zero-expense index funds, while Vanguard offers consistently low expense ratios across many funds.

Are Fidelity index funds as good as Vanguard?

Yes. Many track the same benchmarks and perform similarly over time.

Is Vanguard safer than Fidelity?

Both are large, established firms with strong financial stability and regulatory oversight.

Can I transfer from Vanguard to Fidelity?

Yes, account transfers between brokers are common and typically straightforward.

Which is better for retirement accounts?

Both are excellent. Fidelity may offer more tools, while Vanguard emphasizes disciplined long-term investing.

Do both offer ETFs?

Yes, both firms provide a wide range of ETFs across sectors and asset classes.

Is customer service better at Fidelity?

Fidelity often ranks slightly higher in customer service surveys, especially for responsiveness.

Conclusion

The debate over fidelity vs vanguard isn’t about right or wrong—it’s about fit.

Both companies are leaders in low-cost investing, retirement planning, and long-term wealth building. Fidelity shines in technology, accessibility, and active fund options. Vanguard stands out for its pioneering index philosophy and ultra-low expenses.

For most long-term investors, either platform can serve you well. The key is choosing the one that aligns with your investing style, discipline, and comfort level—and then staying consistent for decades to come.